Learn more about Wellable's all-in-one

employee engagement platform

Learn more about Wellable's all-in-one

employee engagement platform

Many employers offer wellness incentives to encourage employees to engage in wellness programs and adopt healthy behaviors. Often, these incentives are monetary (e.g., direct payments or items with fair market value). Most monetary incentives are taxable, but this may not appear obvious to companies due to the complexity of federal guidelines. This raises the question: how many organizations are appropriately taxing their wellness program incentives?

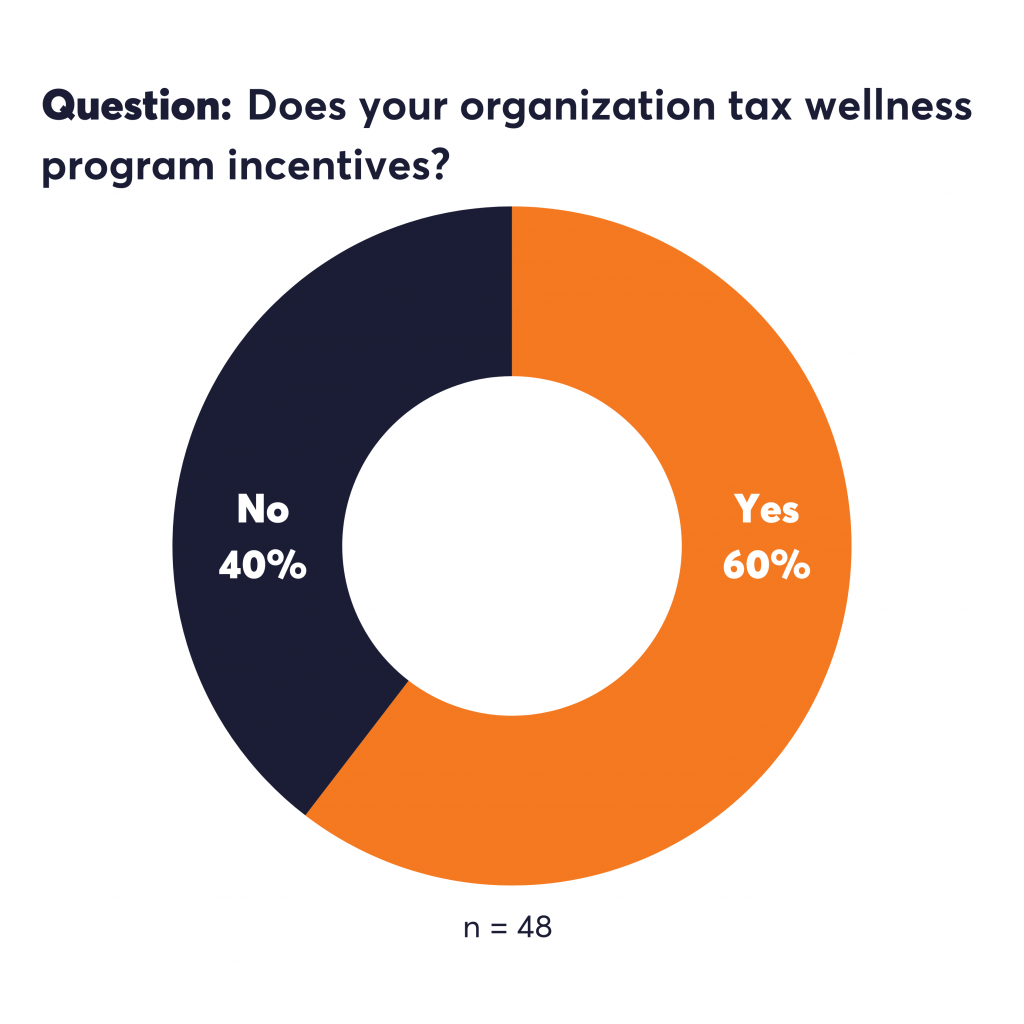

Survey results: Are wellness incentives being taxed?

To answer this, Wellable surveyed human resources and wellness professionals subscribed to the Wellable Weekly newsletter. Sixty percent said yes, while 40% said no.

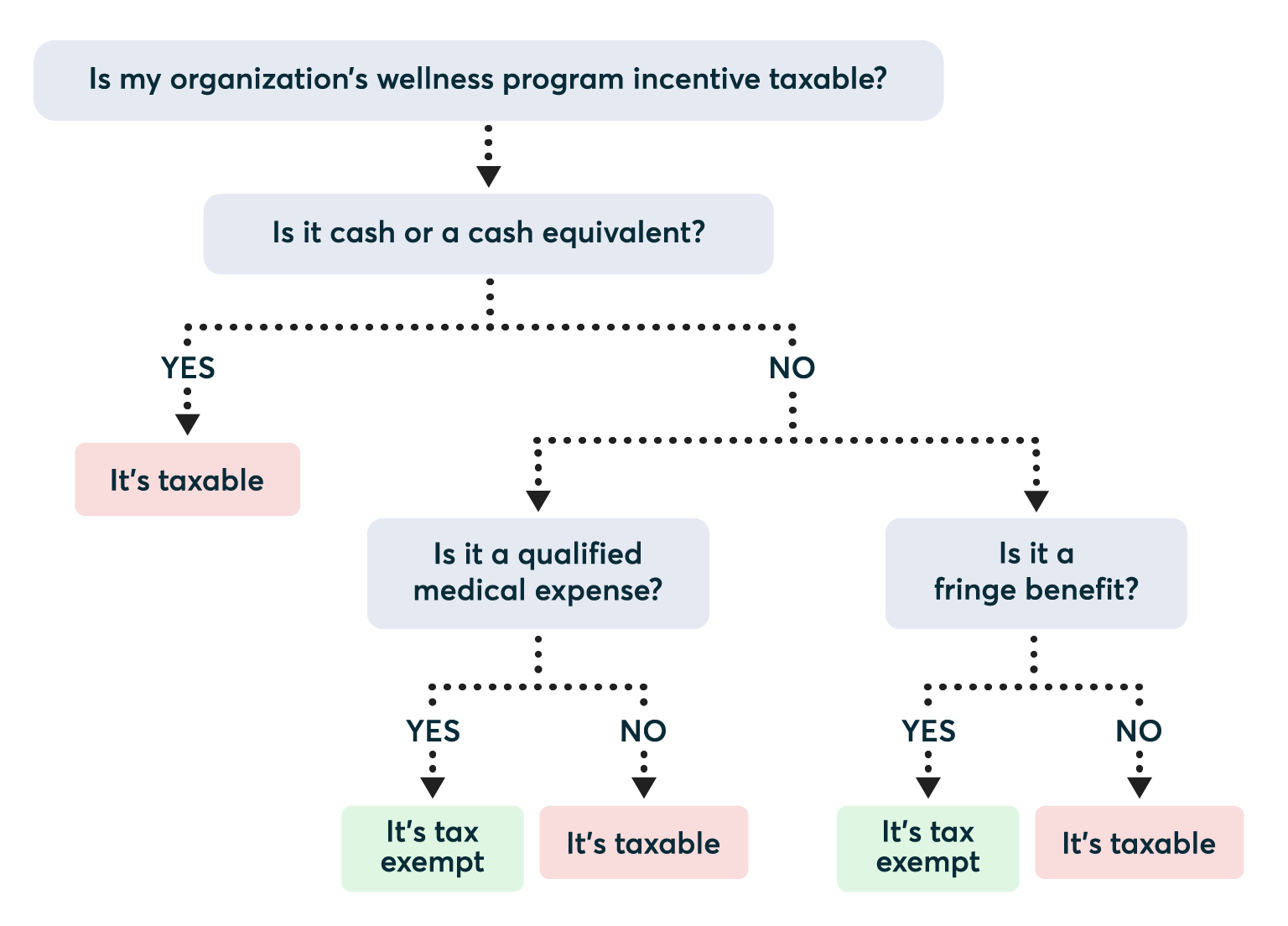

Given that many wellness incentives are taxable, the results probably shouldn’t be so divided. Some organizations might need of a crash course on the taxability of wellness incentives. To address this, Wellable offers a decision tree that provides US companies with a series of questions to determine if a particular incentive is taxable. Once the decision tree is laid out, additional information is provided to simplify the process of answering its questions.

Taxable Wellness Incentives

Cash and Cash Equivalents

Cash equivalents include other assets that are readily convertible into a pre-specified amount, like a $100 gift card. As is noted in the decision tree above, these incentives are always taxable.

Nontaxable Wellness Incentives

Eligible Medical Expenses

According to the sections 105 and 106 of the IRS code, medical care expenses paid either by an employee or their employer are nontaxable. Section 213(a) states that:

Medical care includes amounts paid for the diagnosis, cure, mitigation, treatment, or prevention of disease, or for the purpose of affecting any structure or function of the body.

[Medical care] does not include cosmetic surgery or other similar procedures, unless the surgery or procedure is necessary to ameliorate a deformity arising from, or directly related to, a congenital abnormality, a personal injury resulting from an accident or trauma, or a disfiguring disease.

Some examples of nontaxable medical expenses may include:

- Health club memberships (when prescribed by a doctor to treat an illness)

- Employer contributions to a flexible spending account (FSA), health reimbursement account (HRA), or health savings account (HSA)

- Reduction of cost sharing under a group health plan (e.g., premiums, deductibles, or copayments)

Fringe Benefits

Fringe benefits are typically understood as benefits that are outside a company’s standard health insurance offerings. Many types of fringe benefits are nontaxable (for a complete list, see section 2 of the Employer’s Tax Guide to Fringe Benefits). Some notable examples include:

- Properties or services which have such a small value that accounting for them is impractical (e.g., snacks, water bottles, and t-shirts)

- On-site athletic facilities, as long as they are primarily used by “by employees of the employer, their spouses, and their dependent children

- Qualified employee discounts (these discounts cannot be too large; for a precise account of the rule, check out Section 132(c) of the fringe benefits guide)

Final Takeaways

Seek professional legal or accounting counsel. While the guidance provided here is a good place to start, it is not intended to be exhaustive or a substitute for accounting or legal advice.

Keep employees informed. It is important to let employees know which incentives are taxable and which aren’t. Employees whose taxes are not automatically withheld by their employers must be informed about the taxability of their rewards so that they can pay the proper amount in taxes and avoid legal consequences.

This article was last updated on February 3rd, 2025

-

Share

-

-

-

-